A mortgage banker may offer you a 3-2-1 Temporary Mortgage Rate Buy-down. This program is designed to help lower a borrower’s monthly mortgage payment during the first few years of the loan.

Here’s How It Works

1. The buy-down amount is determined upfront and is the difference in payment between the buy-down rate and the actual note rate multiplied by 12 each year.

2. In a 3-2-1 buy-down, during the first year of the loan, the interest rate is reduced by the full buy-down amount. For example, if the current interest rate is 6%, the first-year rate would be 3% (6% – 3%).

3. During the second year, the interest rate is reduced by 2%. For example, if the note rate is 6%, the second-year rate would be 4% (6% – 2%).

4. During the third year, the note rate is reduced 1%. For example, if the note rate is 6%, the third-year rate would be 5% (6% – 1%).

At the start of the 4th year, the interest rate will return to the original note rate, in the case of our example 6%.

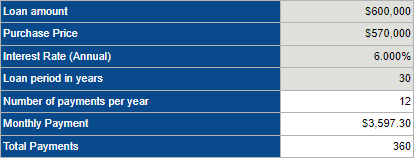

Below are two examples to illustrate the 3-2-1 Temporary Mortgage Rate Buydown with the payments for years 1, 2, and 3.

Example 1

In this scenario, in order to be able to achieve this buydown, the seller or bank would need to credit you $26,122.36.

Example 2

In this scenario, in order to be able to achieve this buy-down, the seller or bank would need to credit you $17,414.91.

In conclusion, the 3-2-1 Temporary Mortgage Rate Buy-down is a valuable option for borrowers looking to lower their monthly mortgage payments during the first few years of the loan. By reducing the interest rate during the early years of the loan, the buy-down can help make home ownership more affordable for borrowers until they are able to refinance if and when the rates go back down.

Discount Point or Buy-down Explained.

A mortgage discount point, also known as a buy-down, is an upfront fee that a borrower can pay to lower their mortgage interest rate. This option may be a good choice for borrowers who plan to stay in their homes for a longer period of time and want to reduce their monthly mortgage payments.

The cost of a mortgage discount point is expressed as a percentage of the loan amount, and the amount of the discount varies depending on the number of points purchased. For example, purchasing one discount point may lower the interest rate by 0.25%.

The key factor to consider when deciding whether to pay for a discount point is the recapture rate of the cost associated with it. The recapture rate is the time it takes for the monthly payment savings to recoup the cost of the discount point. If the recapture rate is sooner than 3 years, paying for a discount point may be a good option.

For example, if a borrower pays $2,000 for a discount point on a $200,000 loan, and the monthly payment savings is $100, the recapture rate would be 20 months (2,000 / 100). In this case, the cost of the discount point would be recouped in less than 2 years.

In conclusion, a mortgage discount point or buy-down may be a good option for borrowers who plan to stay in their home for a shorter period of time and want to reduce their monthly mortgage payment during that period. If the recapture rate of the cost associated with the buy-down is sooner than 3 years, it can provide a quick return on investment for the borrower.

The One-Two Punch

Lending Arena recommends a combination of the 2:1 or 3:2:1 buy-down with a regular mortgage buy-down in order to get the best of both worlds. When shopping for a home, speak to your realtor about asking for as much in closing costs as you can get. For example, if you can ask a seller on a 600,000 to give you 5% in closing costs, you can then use the 30,000 credit towards the above-mentioned buy-downs. Use a portion of the 30,000 for a natural buy-down, and another portion for the 2:1 Buy-down. Let us look at a few examples below.

Punch 1 – The natural buy-down. Let’s assume the market rate is at 6%, now let us spend 10,000 of the 30,000 to buy down that 6% to 5.375%.

Punch 2 – The 2:1 Buy-down. Now, let’s spend 12,856.39 to initiate this program. See below for calculations:

This post was created with our nice and easy submission form. Create your post!